Compliance & Training Manual

McGrath Estate Agents

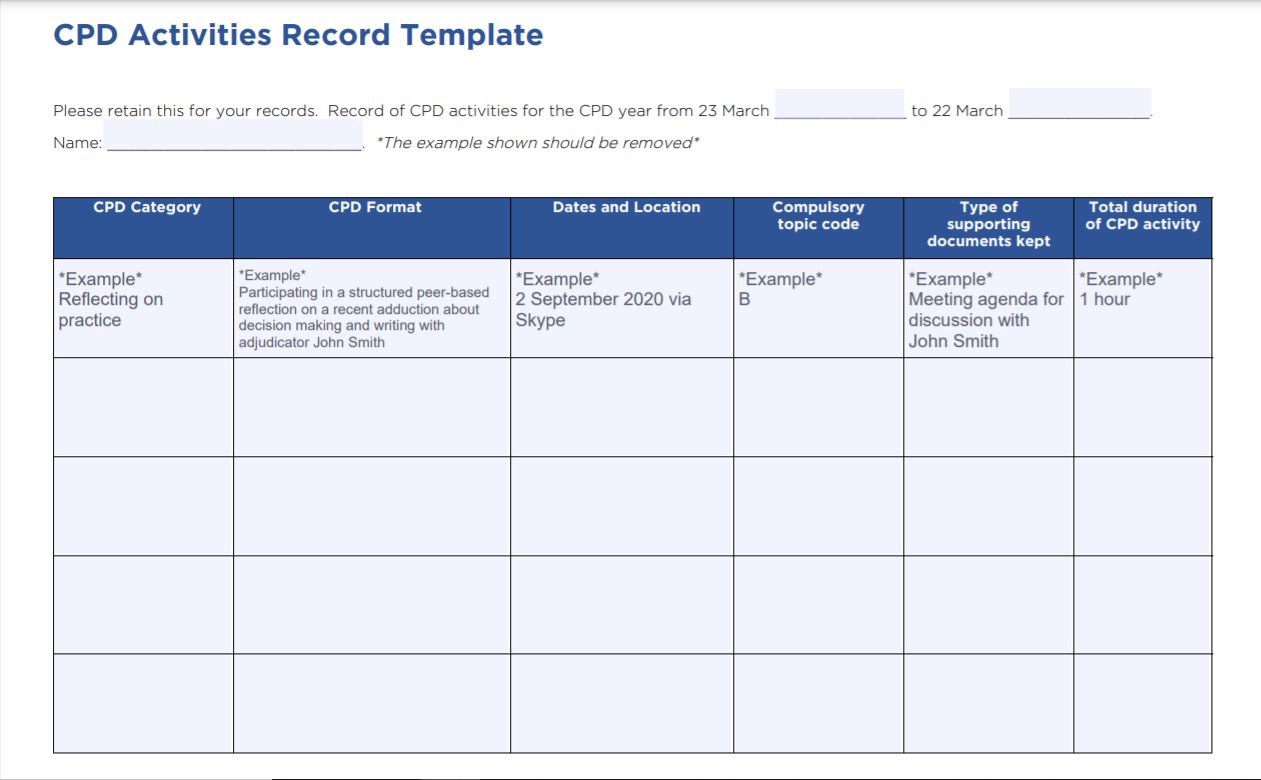

Log Book/ Record Book

To assist with this, please see below for an example of a Log Book/Record pages that can be used to assist with the record keeping:

CPD 2020 Class 1 & 2 Log Book

Licensed Agent Name: _______________________________________ Class 1 [] Class 2 []

License #: _________________

To meet compliance requirements each licensed agent (Class 1 and Class 2) MUST complete three (3) hours of Compulsory Topics (prescribed by NSW Fair Trading) AND three (3) hours of Elective CPD Topics (as noted below).

N.B. Class 1 license holders will need to do an additional three (3) hours of business-related CPD training in the 2nd year of this system (i.e. 2021-2022).

COMPULSORY CPD & ELECTIVE CPD

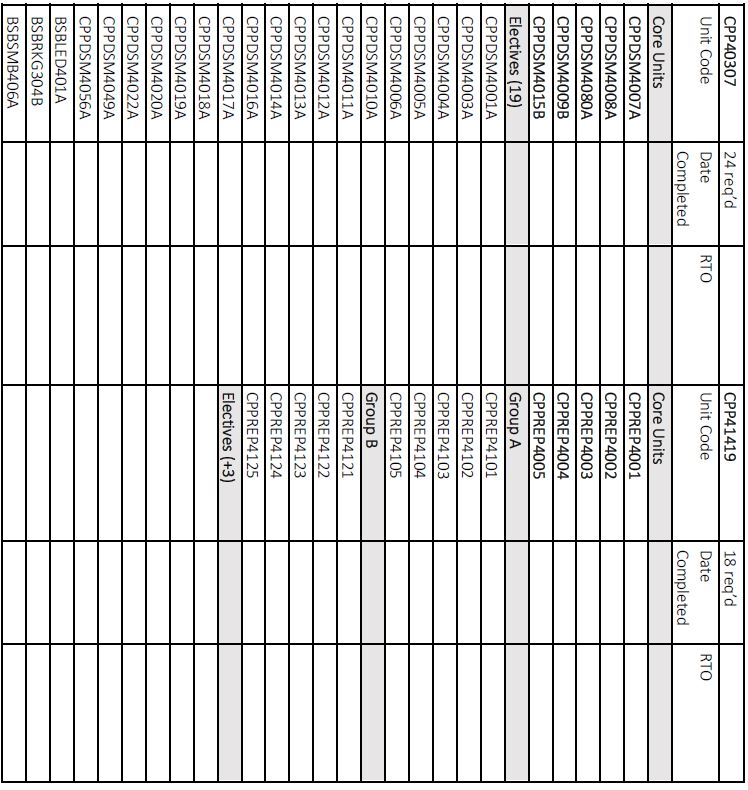

CPD 2020 Assistant Agent CPD Record Book

Assistant Agent Name: _______________________________________ COR # _________________

To meet compliance requirements each Assistant Agent MUST complete AT LEAST three (3) Units of competence from one of the relevant Certificate IV training packages outlined below.

The Statement of Attainment must be issued by the RTO before 22/03/2020, and attached to this Record.

N.B. All Assistant Agents must have completed their Certificate IV course and been issued with the Class 2 license within four (4) years, or they will be required to leave the industry for at least 1 year.

SOA provided to L-I-C on ____/_____/202__ L-I-C signature ______________________________

The Compulsory CPD topics are set by NSW Fair Trading and must be delivered by an Approved Provider.

MRT Training is “an approved provider” for the NSW CPD requirements.

The three (3) topics specified by NSW Fair Trading for this first CPD year are (a) the new Legislation (Residential Tenancy Act, and Property & Stock Agents

Act), (b) the Rules of Conduct, and (c) Risk Management.

Certificate of Registration holders (Assistant Agents) are required to be completing their studies towards having their full license

In order to meet their CPD obligations, Assistant Agents must complete at least three (3) units per year until they have completed the relevant Certificate IV course to gain the full Class 2 License.

This must be completed within 4 years, or those Assistant Agents will be required to “leave the industry” for one year.

Supervision Guidelines

1. Licensee in charge

1.1. A principal licensee must:

1.1.1. ensure that no part of the business is left unsupervised by a licensee in charge

1.1.2. ensure that no more than one licensee in charge is in charge of any one particular part of the business at any time,

1.1.3. ensure that any licensee in charge who is permanently or temporarily unable to properly carry out their duties due to illness, leave or some other reason, is replaced by an appropriate class 1 license holder such that there remains a licensee in charge appointed at all times,

1.1.4. prepare and maintain a document as part of the operational procedures that clearly identifies each licensee in charge relating to the business, the dates on which they were the licensee in charge and, if the licensee has appointed more than one licensee in charge, the part of the business that each person is in charge of, including which trust accounts the person is in charge of; and

1.1.5. ensure that details of every licensee in charge employed by the principal licensee, including the dates they commenced and finished being a licensee in charge, are notified to the Secretary in accordance with section 31(3) of the Act. This includes notifying the Secretary of address of each place of business at which the person discharges their duties as a licensee in charge of the business.

2. Requirement to prepare occupational procedures

2.1. A principal licensee must prepare and maintain operational procedures for the purposes of providing adequate supervision of business processes and employee conduct across the entirety of their business.

2.2. A principal licensee must ensure all operational procedures of the business are reviewed at least once each calendar year to ensure they are sufficiently robust and comply with the law.

2.3. A principal licensee must ensure all persons engaged in the business are familiar with and comply with all operational procedures.

2.4. A licensee must comply with all operational procedures of the business they are engaged in.

3. Trust account procedures

3.1. A principal licensee who employs a licensee in charge must:

3.1.1. ensure that each trust account maintained in accordance with Part 7 of the Act by the principal licensee, in connection with their business as a licensee, has only one licensee in charge who is responsible for and able to authorize withdrawal of money from that account, and

3.1.2 prepare and maintain a document that clearly identifies each licensee in charge and the trust account/s for which they are responsible.

3.2. A principal licensee must prepare and maintain written procedures for the review of trust accounts and daily or next day banking practices with respect to the receipt of trust money.

3.3. Without limiting clause 3.2, the written procedures must ensure:

3.3.1. that each trust account has only one licensee in charge who can authorize the withdrawal of trust money from that account, and details of the relevant licensee in charge and trust account have been recorded for each trust account,

3.3.2. a review of trust account transactions is conducted at least once per calendar month,

3.3.3. the amounts deposited into and withdrawn from the trust account have been verified using the relevant financial institution’s records as source documents,

3.3.4. all persons who have access to the trust account system have separate logins, and their passwords are not shared with anyone,

3.3.5. any adjustments shown in an end of month reconciliation can be explained with evidence,

3.3.6. there are processes for obtaining and documenting the express authorization of a licensee in charge to withdraw trust funds in accordance with the Regulation,

3.3.7. rental and sales money is paid into the appropriate trust accounts, and

3.3.8. rental money owing to a landlord under a residential tenancy agreement (less any authorized expenses) is paid to the landlord at the end of each calendar month, unless instructed otherwise by the landlord.

3.4. A licensee in charge must maintain a record of all cash transactions which includes, at a minimum:

3.4.1. the cash amount received,

3.4.2. the name of the person who received the cash from the payer,

3.4.3. the name of the person who prepared the daily banking of those funds,

3.4.4. the name of the person who deposited the funds in trust at the financial institution, and

3.4.5. the trust account details.

4. Identification check for the purposes of fraud prevention

4.1. A principal licensee must prepare and maintain written procedures for the verification of the identity of a party with whom it is proposed to enter an agency agreement.

4.2 Without limiting clause 4.1, the written procedures must provide for the following:

4.2.1 a process to verify that the identity of a person entering an agency agreement is the owner of the property that is subject to the agreement or, the person has the legal right to act on behalf of the owner,

4.2.2 if applicable, in the case of a person who has the legal right to act on behalf of the owner — where that person is not listed on the certificate of title, the original or a certified copy of the document which confers the power of sale or management on that person must be sighted, and a copy of the document must be retained,

4.2.3 if applicable, where there is no mortgagee listed on the certificate of title, written confirmation of the power of sale or management is sought from all registered owners listed on the title,

4.2.4 where it is not possible to comply with clause 4.2.3, a reasonable attempt must be made to verify the power of sale or management with the registered owner of the property and a record retained of each attempt,

4.2.5 a record must be kept of all documentation relied upon to verify an individual’s identity,

4.2.6 the confirmation of identity check must meet all provisions of clause 4.3 of the supervision guidelines.

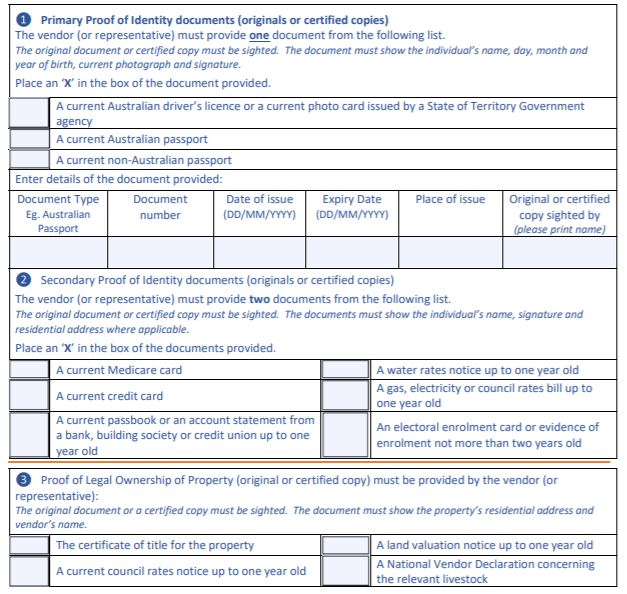

4.3 In verifying the identity of a person, a licensee must sight an original or certified copy of:

4.3.1 a primary proof of identity document,

4.3.2 two secondary proof of identity documents, and

4.3.3 a document providing proof of legal ownership of the property.

4.3.4 in the case of the sale of a business, only 4.3.1 and 4.3.2 apply.

4.4 For the purposes of clause 4.3, a primary proof of identity document is:

4.4.1 a current Australian driver’s license, or

4.4.2 a current photo card issued by a State or Territory Government agency, or

4.4.3 a current Australian passport, or

4.4.4 a current non-Australian passport.

4.5 For the purposes of clause 4.3, a secondary proof of identity document is:

4.5.1 a current Medicare card, or

4.5.2 a current credit card, or

4.5.3 a current passbook or an account statement from a bank, building society or credit union up to one year old, or

4.5.4 an electoral enrolment card or evidence of enrolment not more than two years old, or

4.5.5 a gas, electricity or council rates bill up to one year old, or

4.5.6 a water rates notice up to one year old.

4.6 For the purposes of clause 4.3, a document that is proof of legal ownership of the property is:

4.6.1 the certificate of title for the property, or

4.6.2 a current council rates notice up to one year old, or

4.6.3 a land valuation notice up to one year old, or

4.6.4 a National Vendor Declaration concerning the relevant livestock.

4.7 In verifying a proof of identity document, a licensee must ensure:

4.7.1 the documents are legible and appear not to have been altered in any way, and

4.7.2 there is no discrepancy between the information collected by a licensee and the information contained in the documents, other than a discrepancy that can be explained and supported with evidence, and

4.7.3 the photograph contained in photographic identification documents is a true likeness to the person whose identity is being verified.

5. Ongoing dealings with parties to an agency agreement

5.1. A principal licensee must prepare and maintain written procedures that ensure all communication during the provision of services under an agency agreement is with the owner of the property or the person with the legal right to act on the owner’s behalf.

5.2. Without limiting clause 5.1, the written procedures for ongoing communication must ensure:

5.2.1. persons engaged in the business only use contact details held on the file which have been confirmed to belong to the person who is party to the agency agreement,

5.2.2. if a party to the agency agreement requests to change their contact or bank details, the change of details is confirmed, via an alternative contact method to the way in which the request originated with all parties to the agency agreement.

6. Sale of residential property – selling price and other representations

6.1. Clause 6 is only applicable to the sale of residential property.

6.2. A principal licensee must prepare and maintain written procedures for substantiating any estimated selling price, as defined in section 72 of the Act, that has been provided to a seller or prospective buyer of residential property.

6.3. Without limiting clause 6.2, the written procedures must ensure that the following factors have been considered when determining the estimated selling price:

6.3.1. any sales of comparable properties,

6.3.2. feedback from potential purchasers,

6.3.3. any current or relevant valuations provided in respect of the property,

6.3.4. the characteristics and features of the property,

6.3.5. the methods used to market the property,

6.3.6. any other available factor that may affect the estimated selling price.

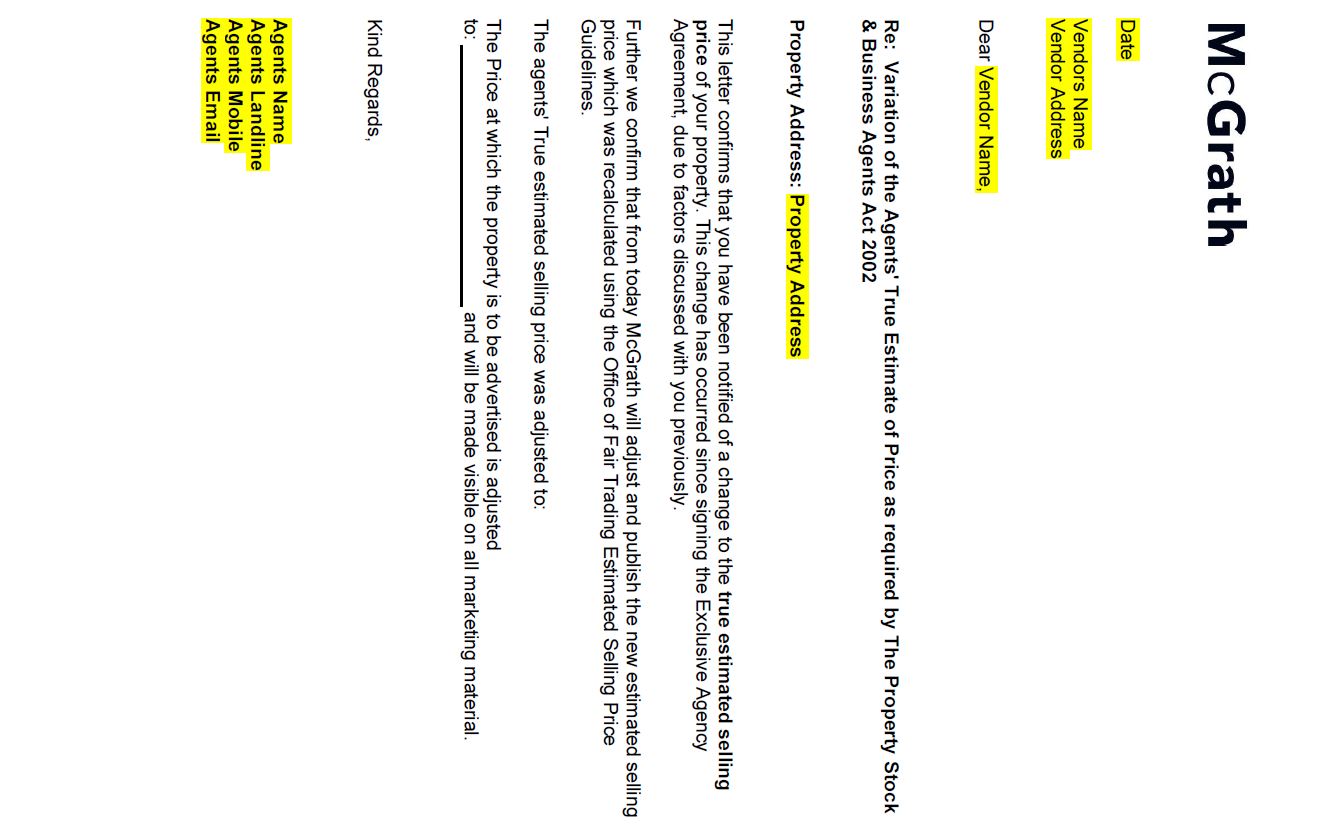

6.4. A licensee must retain a record of information that demonstrates how the estimated selling price was determined to be reasonable.

6.5. A licensee must ensure that the estimated selling price is reviewed at least weekly to confirm it remains a reasonable estimated selling price.

6.6. When changes are made to an estimated selling price, a licensee must ensure:

6.6.1. the change is communicated in writing to the vendor with evidence of how they estimated the revised estimated selling price as soon as practicable, and

6.6.2. the relevant agency agreement is amended to reflect the revised estimated selling price.

6.7. Where there is a difference between the estimated selling price and the actual selling price, a licensee must be able to demonstrate that the difference was reasonable in the circumstances.

6.8. A licensee must ensure that any price statement made by a person engaged in the business is consistent with:

6.8.1. the vendor’s instructions, and

6.8.2. is not lower than the estimated selling price.

6.9. Where a vendor instructs a person engaged in a licensee’s business not to disclose a selling price, a licensee must ensure that the estimated selling price or any other selling price is not disclosed to potential buyers in writing or verbally by any person engaged in the business.

6.10. Where a licensee is responsible for managing the sale of a multi-unit or multi- lot property under an agency agreement, they must comply with the following:

6.10.1. If any price indication is given, it must include the estimated selling prices for the lowest and highest priced properties in each property category expressed by:

a. providing the price ranges for each category, with the low end of the range being the estimated selling price of the lowest priced property in the category and the higher end of the range being the most expensive property in that category; or

b. stating the estimated selling price in the agency agreement of the lowest and highest priced properties for each property category

6.10.2. Any collective marketing of residential units or lots that include a price indication must also advise prospective buyers that there are multiple properties within each category of varying prices

6.10.3. All advertising and marketing must be updated to reflect the value of the current lowest priced lot or unit available.

6.11. A principal licensee must prepare and maintain written procedures that ensure all persons engaged in the business who are involved in the sales process are aware of, and meet, the following requirements:

6.11.1. All advertising material must accurately describe the property concerned and the information provided complies with the relevant agency agreement and legislative requirements in the Act, the Australian Consumer Law under the Competition and Consumer Act 2010 (Cth).

6.11.2. All conflicts of interest must be properly disclosed, as required by Division 4 of Part 3 of the Act, to the clients, and where appropriate, any prospective buyers,

6.11.3. The listing agent engaged to sell the property must be aware of the restrictions on obtaining a beneficial interest in the property.

7. Complaints handling procedures

7.1. A principal licensee must prepare and maintain written complaint handling procedures.

7.2. Without limiting clause 7.1, the written procedures must provide that:

7.2.1. all complaints and the actions taken by the business in response to the complaint are recorded in a register and retained for at least 3 years from the date of receipt or resolution of the complaint, whichever is later, and

7.2.2. complaints relating to financial transactions are reported to a licensee in charge as soon as practicable and are to be supervised directly by that licensee in charge.

8. Employee supervision

8.1. A principal licensee must prepare and maintain written procedures outlining the respective roles and responsibilities of licensees and certificate holders in relation to the preparation and signing of agency agreements, franchising agreements and agency agreements under which two or more licensed agents act in conjunction.

8.2. A licensee in charge is responsible for verifying:

8.2.1. all persons engaged in the business have completed all continuing professional development they are required to undertake according to the Secretary’s requirements issued and notified to licensees and certificate holders under section 20 of the Act,

8.2.2 the applicable work experience requirements in accordance with the Property and Stock Agents (Qualifications) Order 2019 have been met, and

8.2.3. the length of time an individual has been engaged by the agency.

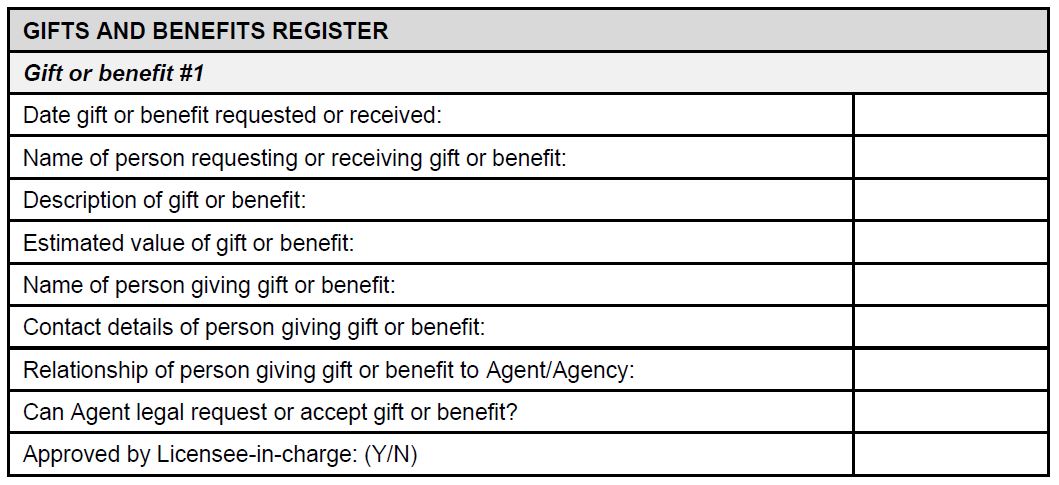

9. Gifts and benefits register

9.1. A principal licensee must prepare and maintain a register of all gifts and benefits received by persons engaged in the business in accordance with section 53F of the Act.

THE LAW

As a general principle, the Agent must act in the best interest of the Principal and, importantly, stand in the shoes of the Principal.

If the Agent receives a gift or benefit while acting for the Principal, that gift or benefit is rightfully the property of the Principal. However, the Agent can earn and retain a benefit if the Agent discloses full details of the gift or benefit to the Principal and the Principal consents to the Agent keeping that gift or benefit.

Section 53F(1) of the Property and Stock Agents Act prohibits an Agent from requesting or accepting a gift or other benefit in circumstances that may reasonably be considered to give rise to a conflict of interest.

There are, however, circumstances where the Agent does not have to disclose the request or receipt of a gift or benefit to the Principal; for example, anything provided by the Agent’s employer, anything provided in accordance with the terms of an agency agreement or from a client as a gift in gratitude for services provided under an agency agreement, if the gift or benefit is of a kind prescribed by the Property and Stock Agents Regulation or anything with a value less than the prescribed amount in the Property and Stock Agents Act (see section 53F(2)(c) and section 53F(2)(d)).

Schedule 1, clause 21 of the Property and Stock Agents Regulation imposes a limit of $60 on the value of gifts and benefits. Therefore, if the individual gift or benefit does not exceed $60, the Agent can request or accept that gift or benefit without disclosing it to the Principal.

AGENCY POLICY

The Licensee-in-charge will create and maintain a Gifts and Benefits Register and this register will be made available to all Agents and other employees of the Agency and those engaged in the Business.

All Agents and other employees of the Agency and those engaged in the Business will record all gifts and benefits in the Gifts and Benefits Register.

All Agents, and other employees of the Agency and those engaged in the business will not request or accept gifts or benefits without first checking to see whether they are able to do so under section 53F of the Property and Stock Agents Act 2002 (NSW).

All gifts or benefits requested or accepted must first be approved by the licensee in charge.

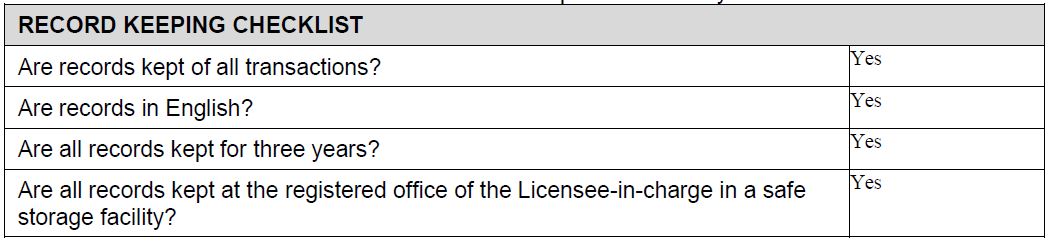

10. Record keeping

10.1. A licensee in charge must maintain records showing evidence of:

10.1.1. regular reviews of operational procedures, and

10.1.2 any non-compliance with the operational procedures by persons engaged in the business

10.2 A licensee in charge must be able to produce all documentation relevant to clauses 1-10 of these supervision guidelines to an authorized office in accordance with section 105 of the Act.

10.3 All records relevant to clauses 1-10 must be kept for at least 3 years.

.

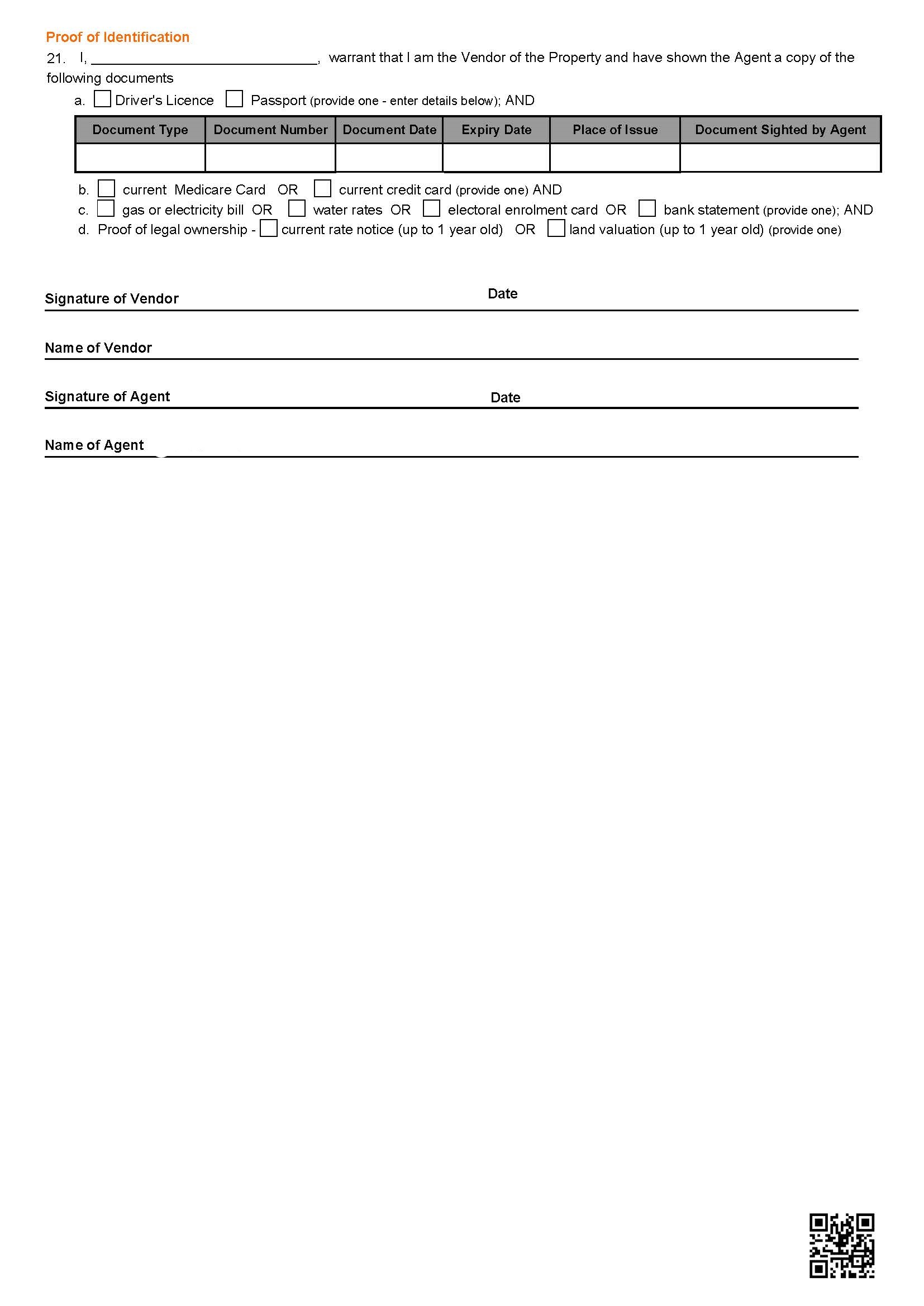

Agency Agreement

.

.

.

.

.

.

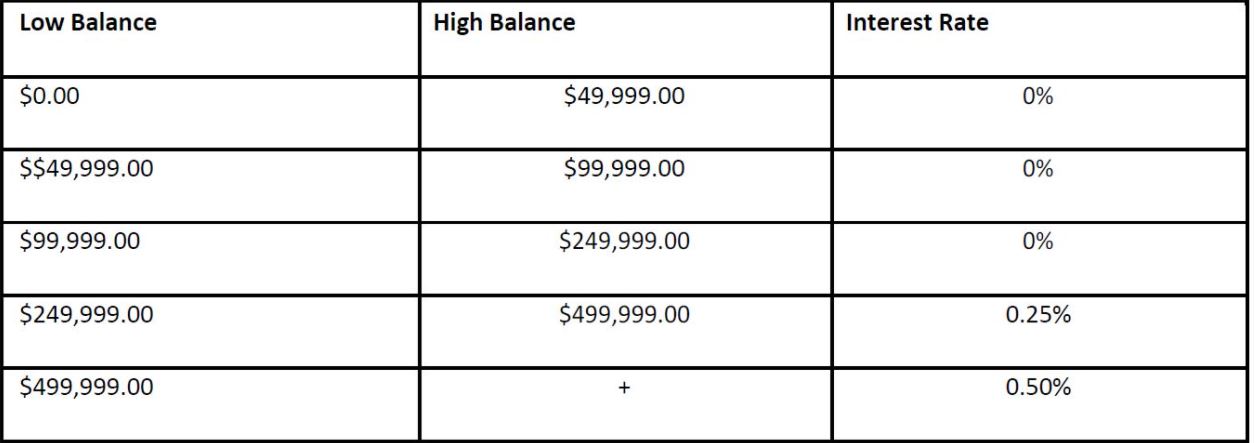

Investing The Deposit

Important: Deposits under $250k WILL NOT BE INVESTED.

Please check your letters are current outlining this information to your clients:

Given the current all time low interest rates – Macquarie Bank current interest rates are noted below.

As illustrated anything below $250k earns $0.

.